Although I am a personal development blogger by profession, I am in no way a mental health professional. See my disclaimer for more info.

Are you tired of worrying about your finances? This post will teach you how to be financially free!

Are you at that point where you’re just OVER it? Stressing all the time about your financial situation?

I get it. I find myself in the same boat as a young adult. I’ve taught myself about the importance of saving, budgeting, and smart shopping, but you really don’t know the consequences of poor financial habits until you experience them yourself.

While I go through this journey of healing my relationship with money, I wanted to share my experience and knowledge with you. In this post, I’ll show you some of the BEST tips I’ve learned over the years to improve your finances. Because even though I’m not perfect, there are some things I’ve been implementing that have made a HUGE difference in my financial life.

This post is all about how to be financially free.

What is financial freedom?

First, you need to know what it really means to be financially free.

To be financially free means to:

- have control over your finances

- have little to no debt

- eliminate stress over money

When you’re financially free, you escape the worries that can usually come with money. You should strive to reach financial freedom if you no longer want to stress about paying bills or anything else related to your finances.

I’m sure we all want to be at point, so keep reading to learn more!

How to Be Financially Free:

1. Stop impulse buying

When you buy something impulsively, you buy it without actually planning to buy it.

For example, say you go to the store for some toothpaste and mouthwash.

You find these 2 items and put them in your cart, but on the way to the register, you see a shirt you like. You didn’t plan on buying it, but you can’t resist the temptation to put it in your cart.

So you buy it along with the 2 things you were actually planning to buy in the first place.

This is impulse buying.

Do you see how this can become a problem over time?

If you continue to impulse buy, you’ll see money constantly leave your bank account. Money that you could instead put toward important savings goals like paying off credit card debt or student loans.

How to stop impulse spending

Quitting your impulse spending depends on how you normally shop.

If you tend to buy things online, I suggest limiting your digital access to your cards. Remove them from the notes app on your phone, Autofill, and any type of mobile wallets (Apple Wallet, Google Wallet, PayPal, etc.)

You should do this because if you have quicker, easier access to your cards, you’ll be more likely to buy something without planning to. I started doing this and I’ve seen major changes to my DoorDash addiction.

Alright, that’s how you stop impulse spending if you normally shop online. If you’re more of a typical shopper, some may argue it’s harder.

It can be more difficult to avoid impulse spending in-person because the item is right in front of you, not online.

Here’s what you can do: if you see something you want, put it in your cart.

Yes; put it in your cart and continue to shop around for the items you originally went in the store for. Then, once it’s time to head to the register, decide whether you really want to buy the item.

Ask yourself some questions:

- “How can I use this in my daily life?”

- “Will this improve my mental, emotional, physical, or financial health?”

- “How often will I use this?”

- If it’s on sale:

- “Would I buy this if it wasn’t on sale?”

- “How much do would I be willing to pay for this?”

- If using a credit card:

- “Will I earn travel points for this purchase?”

- “Will I get (further) into debt by buying this?”

- “Would I buy this if I had the money instead of using a credit card?”

If you can answer these questions in a smart way, it’s probably a good decision to buy the item.

2. Save in a high-yield savings account (HYSA)

If you haven’t started saving your money yet, now’s the time!

You’re probably used to saving your birthday and Christmas money in cash form, but you’re making a mistake by doing this.

When you save your money in cash, in a checking account, or even in a traditional savings account, you earn little to nothing on that cash.

You’re preventing yourself from earning free cash on money that you’re already saving!

The easiest way to start is by saving in a high-yield savings account (HYSA).

what is a high-yield savings account?

A HYSA is similar to your traditional savings account that you open with your bank. The main difference between the 2 is that you earn a much higher return on your money with a HYSA.

Usually, with a regular savings account, you have a 0.01% interest rate. This means you earn next to NOTHING on the money that you keep in your account.

Let’s put things into perspective.

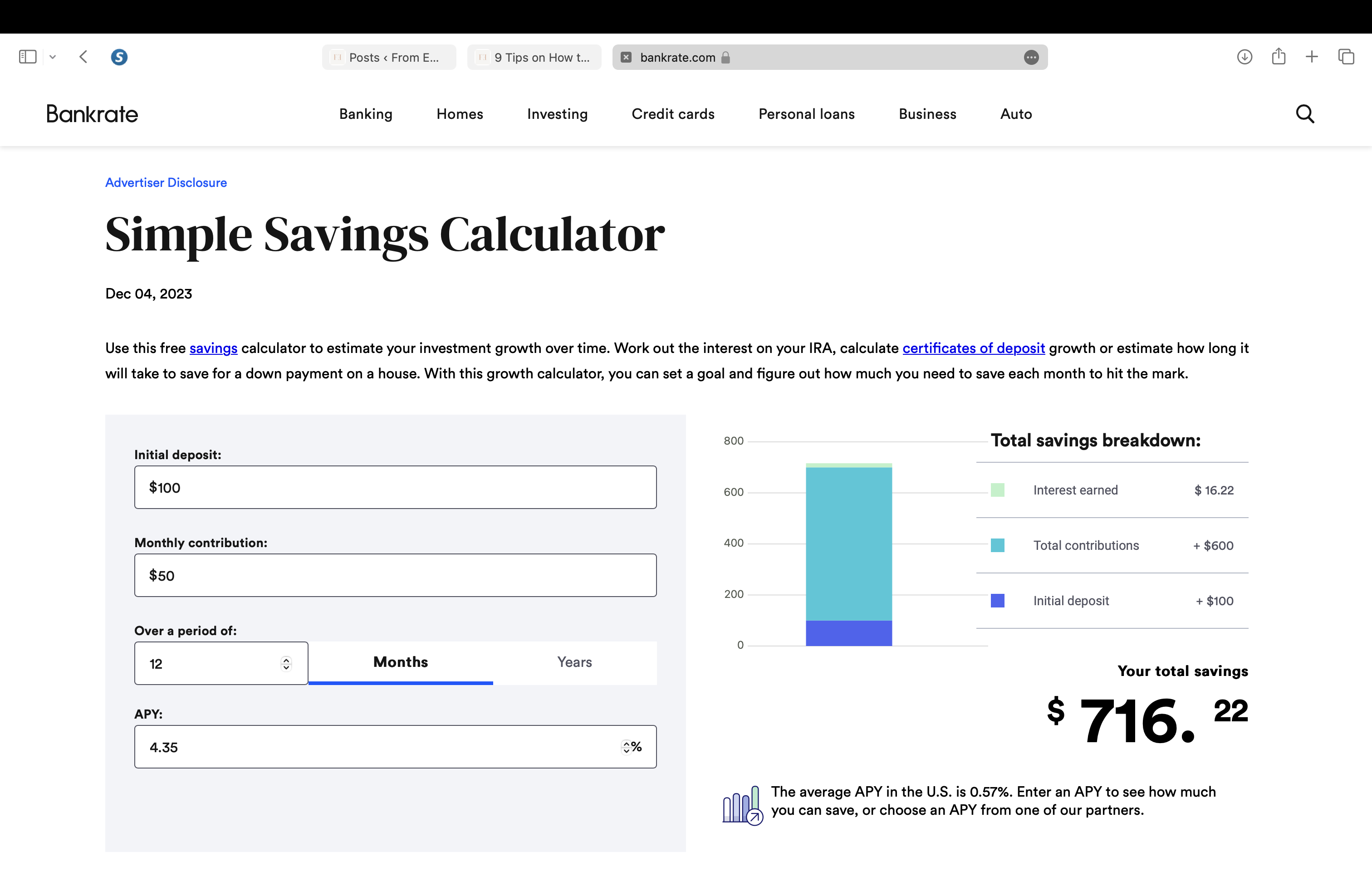

If you put $100 in a Chase savings account (with a 0.01% interest rate) and put $50 in it every month for a year, you will end up with $700.04 at the end of those 12 months. That might sound good, but it can get even better.

Now, let’s do the same thing with a high-yield savings account. If you put $100 in a Discover HYSA (with a whopping 4.35% interest rate) and put $50 in it every month for a year, you will end up with $716.22 at the end of those 12 months.

That’s a $16.18 difference — just from opening a HYSA instead of a traditional savings account.

You might be thinking, “What’s the catch?” For the most part, there’s truly no catch. You really do get a better return on your investment!

I will say, though, if you make more than $10 in interest from your savings account, you must report that money on your taxes.

I am no tax professional by any means, so please consult with a CPA or other tax professional for tax information.

best high-yield savings accounts

To get started with earning more on your money, check out these high-yield savings accounts:

- SoFi (must have direct deposit set up for full interest rate): up to 4.60%

- Marcus: 4.50%

- Discover: 4.35%

- Capital One: 4.35%

- Ally Bank: 4.35%

- American Express: 4.35%

We’re not done yet! Have you heard of an emergency fund?

what is an emergency fund?

An emergency fund is a type of bank account that you go to when something unexpected happens like a big medical bill or when you lose your job.

An emergency fund should include things like money for:

- Food

- Water

- Utilities

- Healthcare

- Housing

- Transportation

Remember that your emergency fund should only include money for needs, not wants.

Like an emergency credit card, you should never spend the money in this account unless you absolutely need to. It’s not an account that you use whenever you run out of money in your normal budget.

Make sure you separate it from all of your other accounts!

how much money should you keep in an emergency fund?

You should keep at least 3 to 6 month’s worth of living expenses in your emergency fund. Calculate your living expenses (listed above) and multiply them by 3 to know how much to contribute to this account.

For example, say your living expenses are $8,000 every month. Multiply that by 3 to get $24K as your emergency fund total.

free self care activities list

Would you like a free self care activities list?

Along with being financially free, it’s important to practice self care. To help, I created a FREE list of 81 self care activities that you can enjoy.

To get the list, simply click here.

3. Pay off debts

Next, try to pay off all debt in your control. I say “in your control” because some types of debt are harder to pay off than others.

There are all sorts of loans, like:

- Auto loans

- Mortgages

- Student loans

- Credit cards

- Business loans

You can’t be financially free if you are constantly worrying about these debts, so you need to make a plan to pay off these loans.

This is called a debt payoff plan. In yours, you need to include important details like interest rates, loan terms, and balances.

Once you start paying off your debts, you’ll start to feel a sense of relief as you work toward being financially free.

4. Stop spending your money before you get it

This one is hard! I know you might be wondering, “How the heck do you spend your money before you even get it?”

What I mean by this is, you need to stop planning what you’re going to do with money that you’re expecting to get in the near future.

For example, if you’re expecting a refund, reimbursement, or paycheck, do NOT make any plans to spend that money until you actually see it hit your checking account.

You’ll be stressed out if your plans are ruined because something happened to the money that you expected.

Also, stop relying on credit cards and payment services like AfterPay and Klarna to buy things!

These usually have high interest rates and you end up spending more money by using these than you do by buying your items with cash. Just be patient and buy things with the money that you actually have.

Plus, it feels so much more satisfying to do it this way than to rely on a loan to get the things you want.

5. Make (and stick to) realistic budgets

The keyword here is realistic. I’m making this a big deal because it’s too often that we make a budget that isn’t realistic.

Let’s be real: why are you constantly making room in your budget for groceries if you never cook? Seriously — it’s a waste of both money and food.

how to make a realistic budget

It’s time to start making realistic budgets.

To make a budget that truly works for you and your finances, you need to take a look at your spending habits and expenses. Look at your credit card and checking account statements and see where the majority of your money goes.

Is it:

- food

- entertainment

- charity

- savings

By looking at this information, you really get a better idea of where your money goes. This will help you make a more realistic budget.

free budget sheet

Are you ready to be financially free?

This FREE budget sheet is perfect for you if you’re serious about getting your finances together. Use this sheet to track all of your fixed and variable expenses, and know exactly where your money is going.

6. Stop loaning money to other people

It’s time to be smarter about who you loan money to; stop just giving money out left and right. I understand if there are special cases (emergencies and such), but for the most part, people probably aren’t paying you back anyway.

Then, you’re losing money that you could’ve used to pay your bills, pay off debt, or save toward a big savings goal.

So, from now on, be more mindful about who you loan your money to, and when you do it.

If you know that the person who is asking for some money is not very likely to pay you back, don’t even bother to give them anything. I know that sounds harsh, but I’m sure you’d rather protect your mental health and finances, right?

Also, be smart about the timing of your loans.

If you’re already struggling to pay your debts, don’t bury yourself deeper into the hole by giving money away. You’re only making it harder on yourself! Just don’t do it.

The next time someone asks for some money and you don’t want to give it to them, tell them exactly that. It’s that simple. You don’t have to explain any further!

I recently heard from someone along the lines of, “If they ask for $10, they’ll ask for $100!” That’s so true! If someone asks for an amount of money as small as $10, that’s a sign that they’re probably not doing very well financially.

And trust: they’ll come back asking for more. So, be smart about how and when you loan money to others. If you’re on your journey to be financially free, it’s probably best to not loan to all (from or to others).

7. Live below your means

It seems like too often nowadays we’re trying to buy all these luxurious and materialistic things just to impress others.

But do you fulfilled when you buy these things? Do you feel something when that money leaves your checking account?

If you find yourself buying materialistic, trendy items, it’s a good idea to take a step back and reevaluate your financial habits.

When you live above your means, you spend money on things that you can’t necessarily afford. More importantly, you indulge on things that you really don’t need.

You’re basically trying to live a lifestyle that doesn’t fit in your financial situation.

For example, you’re living above your means if you’re barely making ends meet by trying to live in a luxury apartment with a retail job.

Sorry, but that’s just not cutting it. You need to start living below your means if you truly want to be financially free.

To live below your means, you need to be willing to give up certain things to see your return on investment in the future.

For example, you might live in a slightly less aesthetically pleasing apartment now.

But in about 2 to 3 years, you’ll be able to comfortably afford that luxury apartment you’ve been dreaming of. You can even make small financial changes to help live below your means.

You can:

- Make coffee at home

- Eat at chain restaurants

- Have a smaller number of subscriptions

- Try DIY projects

- Buy second-hand clothes

I get it — living below your means may not seem all that fun in the moment. You’ll definitely appreciate it in the future when you get to live your “dream life.” It all starts with some discipline and self control!

8. Track your spending

A financially free person will always track their spending and know how much money they’re spending throughout the month.

You should track every expense so you can get a better idea of what categories of finances you’re spending money on the most.

This is also a huge timesaver when it comes time to file your taxes because you have all of your purchases on one sheet, rather than having to scramble through all of your checking account and credit card statements.

Tracking your spending can help you stay on track with your budget.

When you make a budget, you usually have a specific amount of money that you want to spend in a certain category (like dining or entertainment). Tracking your expenses can make sure that you don’t pass that amount!

9. Set money goals

There’s no journey without an endpoint in mind.

When I say “set money goals,” I don’t mean generic ones like “become a millionaire.” No; I’m talking about more specific, actionable money goals, like:

- Pay off credit card in 7 months

- Pay off student loans in 23 months

- Fill emergency fund to $30K in the next 13 months

These goals should be specific to you and your financial situation. Make sure that they are so specific and actionable that you can’t help but to actually take the steps to reach them.

They should have clear amounts and timeframes so you can reach them more efficiently.

That also applies to any other type of goal. A goal can’t be general; or else, you’ll be less likely to reach it because you don’t have an action plan to follow.

How to Be Financially Free

Let’s recap.

In this post, we talked about how to be financially free in 9 steps:

- Stop making impulse purchases

- Pay of ALL debt (if possible)

- Save in a high-yield savings account (HYSA)

- Stop spending your money before you get it

- Live below your means

- Quit buying things for others

- Make (and stick to) realistic budgets

- Track your spending

- Set money goals

When you start implementing these tips in your financial life, you’ll start to see a difference in your financial habits. With these tips, you will be on the right path financial freedom!

Please remember to take time to take care of yourself! For free self care activities, check out this post: 7 Fulfilling Free Self Care Activities for Your Next Self Care Sunday

In the midst of chaos, don’t forget to smile,

DeMarcus – your self care buddy

PIN IT FOR LATER:

This post was all about how to be financially free.

This high yield savings pays off for sure !

I definitely agree, Khadijah. I’m looking forward to building smart financial habits, and saving in a HYSA is one of my top money goals. Thanks for reading!